Every sole proprietor officially operating in Estonia faces the need to pay taxes. One of the key types of taxation is income tax. The rules for which are regulated by special legislation.

This article covers the basics of calculating, and paying income tax for sole proprietors.

Basic Provisions of Income Tax

Let’s review the basic provisions of income tax in Estonia.

What is income tax?

Income tax is a mandatory payment levied by the state on the income of individuals, including sole proprietors. Its purpose is to replenish the state budget from the profits earned by individuals through their activities.

Who is obligated to pay income tax?

All registered sole proprietors are obligated to pay income tax, regardless of the amount of income they receive. This applies even if your business is temporarily suspended or closed. Previously earned income is subject to taxation.

What is the calculation procedure? Income tax is calculated annually based on the entrepreneur’s total income for the previous calendar year. To accurately calculate the final tax amount, the tax rates in effect during the tax period are taken into account.

Income Tax Rate

According to current legislation, the income tax rate in 2025 is set at 22%. It is important to note that this rate applies to all types of income from entrepreneurial activity.

Deducting Expenses from the Taxable Base

Law allows entrepreneurs to incur certain expenses directly related to running a business. By doing so, they can reduce their taxable base. However, only entrepreneurs registered in the commercial register have the right to take advantage of these deductions.

Income Declaration and Income Tax Calculation

It is important to declare income accurately and on time. As we will discuss in the next section.

When and how to file a declaration?

A sole proprietor is required to file an annual declaration of their income from entrepreneurial activity. This is done by submitting a special form, “Form E.” This form is submitted at the same time as filing your personal income tax return (“Form A”) with the Tax and Customs Board.

It is important to remember that the return must be submitted no later than April 30 of the year following the reporting tax period. The form can be completed and submitted online through the e-MTA electronic services system.

Requirements to File

Even if your business income is below the tax-exempt minimum or does not exist at all, filing a return remains mandatory. The same applies if your company ceased business operations during the reporting period.

Calculating and Paying Income Tax

After you submit your return, the Tax and Customs Board will independently calculate the amount of income tax due. You will then receive an official notice stating the exact tax amount. This must be received no later than thirty days before the payment deadline, which is no later than September 1.

You can review the details calculations by viewing the relevant information on the information page of the electronic annual tax filing system. The amount paid in person must be paid no later than the required due date of October 1 of the current year.

Furthermore, the Tax and Customs Department issues refunds for overpaid amounts of this tax. This happens also no later than October 1.

Income Tax Advance Payments

In addition to the mandatory main payment, there is a system of advance payments. This system is designed to evenly distribute the financial burden throughout the year.

Who is required to make advance payments and when?

Advance payments are required by all sole proprietors who received income from their business in the previous tax period. Part 1 of Article 47 of the Income Tax Law explains this. The amount and deadline for payment depend on a number of factors. The most important of which is the amount of your tax liability for the previous year.

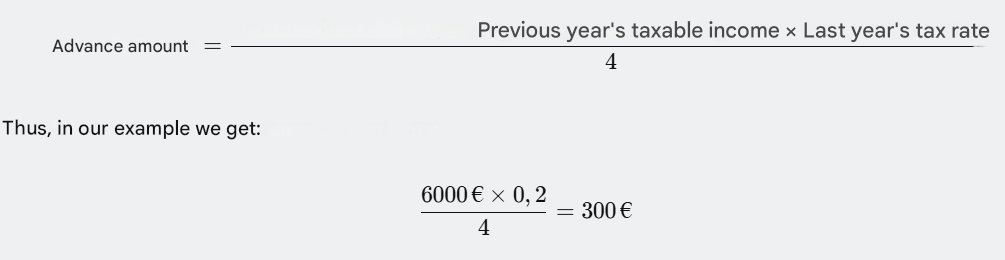

Advance payments are made twice a year – in September and December. The amount of each individual payment is determined as a quarter of the total tax assessed for the previous twelve months.

For example, suppose that last year the taxable income of a sole proprietor was €6,000. And the income tax rate was 20%. Then, each individual advance payment next year would be:

Two equal payments of €300 each would be required for the third and fourth quarters. This would bring the total advance payments for the year to €600.

Exemption from Advance Payments

There are a number of circumstances that do not require payments:

- the first tax period of business activity;

- if the lump sum payment does not exceed the established minimum amount (e.g., €300);

- no taxable income in the previous tax period;

- registration of the enterprise as a temporary or seasonal business;

- temporary suspension of the organization’s business activities.

Circumstances may arise that will lead to a decrease in the expected income. The entrepreneur may submit a request to the department to reduce or waive the payment. It is recommended to submit the application at least one month. Before the expiration of the established deadline.

Conclusion

Knowledge of income tax principles and procedures is an essential aspect of successful entrepreneurship. Properly completing documents and paying required fees on time helps avoid fines. It also helps prevent problems with government agencies. Every individual entrepreneur is responsible for monitoring legislative changes. They must respond promptly to any developments.